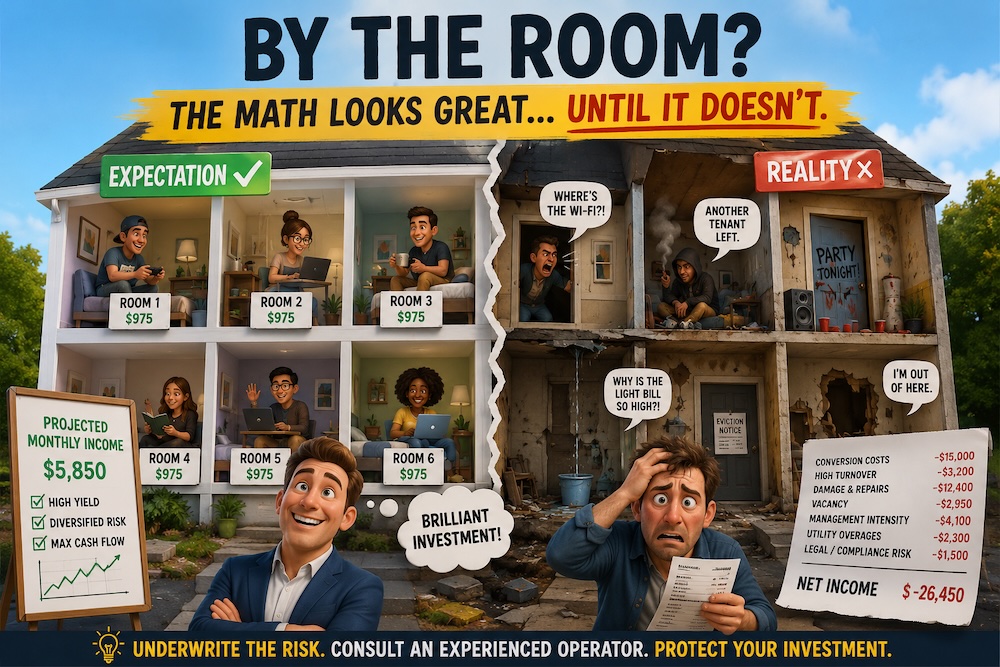

Renting a house by the room can look great on a spreadsheet. Take a larger single-family home, add bedrooms, lease each room separately, and the projected gross rent may appear higher than a traditional lease. In theory, that can create better yield. In practice, it often an operational nightmare and a lower NOI.

This is not to say room rentals never work. Shared housing is a real trend. In 2023, a record 6.8 million U.S. households shared housing with unrelated housemates, roommates, or boarders. Housing affordability is part of the reason: Harvard’s Joint Center for Housing Studies reported that 22.4 million renter households were cost-burdened in 2022.

The demand exists, but only with the right property, in the right sub-market, in the right city.

We are seeing more owners who purchased larger homes, spent $10,000 to $20,000 converting them into six- or seven-bedroom room-rental properties, and are now trying to move back to traditional leasing. In many cases, the owner is spending another $10,000 to $20,000 or more to undo the conversion, repair heavy wear and tear, and make the property attractive to a conventional renter again.

The underwriting mistake is usually simple: the deal only works if every aggressive assumption proves true.

Room-rental underwriting often assumes high occupancy, quick room turns, low conflict between unrelated tenants, limited damage to common areas, manageable utility usage, and a steady supply of qualified renters. But if two rooms are vacant, if one tenant creates issues for the rest of the house, or if common-area wear accelerates, the “higher yield” can disappear quickly.

There is also an exit problem. A house modified for room rentals may not show well to the broader tenant pool. Extra bedrooms, locked interior doors, makeshift layouts, and overused common areas can reduce marketability. The owner may have converted the house for one tenant profile, only to discover that the more stable long-term tenant profile wants the original floor plan back.

Local rules matter too. Texas has statewide occupancy rules, and cities or HOAs may have additional restrictions. In other markets, co-living operators have faced direct challenges from local unrelated-occupancy ordinances. That does not mean every by-the-room strategy is illegal or bad; it means the legal and operational risk should be underwritten before closing, not after the property is already converted.

The bigger lesson is this: if an investment only works because of a novel use case, the deal may not actually work.

Good rental investments should have multiple exits. Could the home work as a traditional long-term rental? Could it sell to an owner occupant? Could it compete without an unusual operating model? If the answer is no, the investor is not just buying a house. They are buying a highly specialized business plan.

Before purchasing, talk to an experienced local operator. A good property manager can help evaluate realistic rent, tenant depth, leasing velocity, make-ready cost, maintenance exposure, HOA restrictions, and the likely exit strategy.

A better question than “What is the highest rent I can project?” is “What is the most durable income this property can produce with the least operational fragility?”

That question can save investors a lot of money.